Seafood Industry Consolidation Trends – Seafood Expo Global 2026 Finance Forum with Ignacio Kleiman

At the 2026 Seafood Expo Global in Barcelona, Ignacio Kleiman, Managing Partner of Antarctica Advisors, spoke at the Marine Money Seafood Finance Forum on Wednesday, April 22, providing key insights into the evolving structure of the global seafood industry.

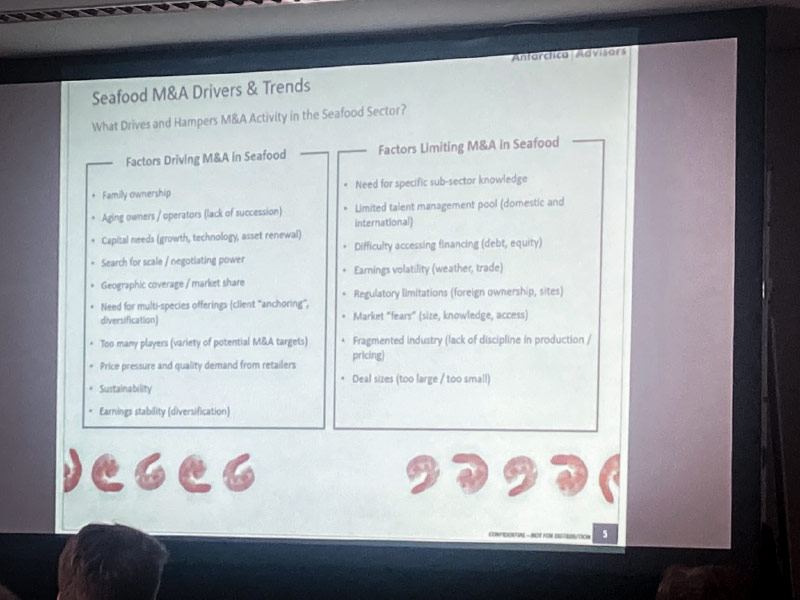

The session, which was later reported on by Undercurrent News, highlighted how fragmentation, operational complexity, and increasing capital requirements are accelerating consolidation across the sector.

Kleiman emphasized that seafood remains one of the most complex segments within the broader protein industry. “The only time that seafood becomes seafood is when that shrimp and lobster and whitefish and tilapia… come together,” he noted, pointing to the diversity of species, supply chains, and end markets that define the industry.

This complexity—combined with varying regulatory frameworks, cultural preferences, and sourcing dynamics across regions—has historically slowed consolidation compared to other protein categories. However, that dynamic is shifting.

“The dynamic is … perfect for M&A,” Kleiman explained, as rising costs tied to automation, efficiency improvements, and supply chain optimization are pushing smaller operators to seek partners or consider exits.

Scale is becoming increasingly important as well. Large retail customers are simplifying their supplier bases, favoring companies that can provide consistent, multi-species offerings across geographies. This trend is rewarding larger, diversified platforms and driving further consolidation.

At the same time, Kleiman noted that seafood remains a knowledge-intensive industry where operational expertise is critical to success. “You can go and buy a beautiful machine, but if you do not have the market knowledge, it’s just not worth the money,” he said.

Access to capital remains another challenge, as lenders often struggle to fully understand the industry’s volatility and operational nuances. Despite these hurdles, the long-term outlook remains highly attractive, supported by growing global demand for protein and the opportunity to unlock value through strategic acquisitions.

“There are many targets, so you can choose your flavor, size and location of your acquisition,” Kleiman said. “Because of this, there is what we call a consolidator class that is emerging.”

Drawing on Antarctica Advisors’ experience advising clients across the seafood value chain, Kleiman encouraged companies pursuing transactions to focus on strong financial performance, operational readiness, and realistic valuation expectations. He also highlighted the importance of flexible deal structures to align incentives and bridge gaps between buyers and sellers.

As consolidation continues to reshape the seafood industry, Antarctica Advisors remains actively engaged in supporting clients through complex transactions—helping them navigate market dynamics, identify strategic opportunities, and create long-term value.

Undercurrent News:

https://www.undercurrentnews.com/2026/04/23/strategic-consolidators-aim-sights-at-global-seafood-industry/