Four finance experts with deep roots in Alaska’s salmon industry give their predictions for what’s to come as the sector retrenches after several difficult years.

The 2025 salmon season in the US state of Alaska delivered solid, if unspectacular, results for the remaining players still standing after a tumultuous few years in the industry.

The outcome is providing a measure of stability to a sector that has undergone a massive wave of change and consolidation over the past two years, according to four top Alaska-focused mergers and acquisitions (M&A) experts who spoke with Undercurrent News recently.

Salmon is perhaps the most iconic species in the US state that accounts for more than half of the nation’s total seafood production. But the industry has been beset by turbulence, as Undercurrent has reported, resulting in the pullback of Alaska behemoth Trident Seafoods and the disappearance of stalwarts like OBI Seafoods and Peter Pan Seafoods.

“If it was another tough year, there were people who would have been forced to exit one way or the other. Either they wouldn’t be able to get financing or their bank was going to force them to do some things they may not want to do,” a senior banking executive serving Alaska’s seafood sector told Undercurrent.

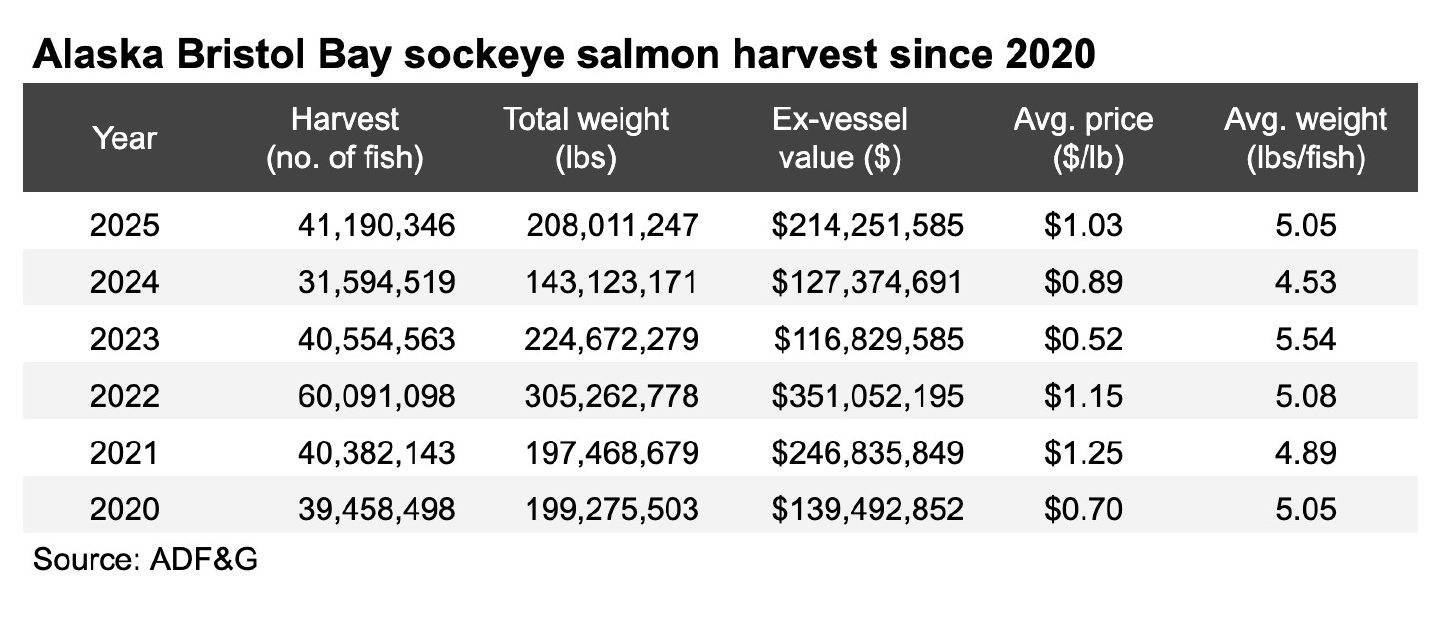

Alaskan fishermen harvested 41.2m sockeye in Bristol Bay in 2025, up 30% from 2024 and 18% above the preseason forecast, as reported by Undercurrent.

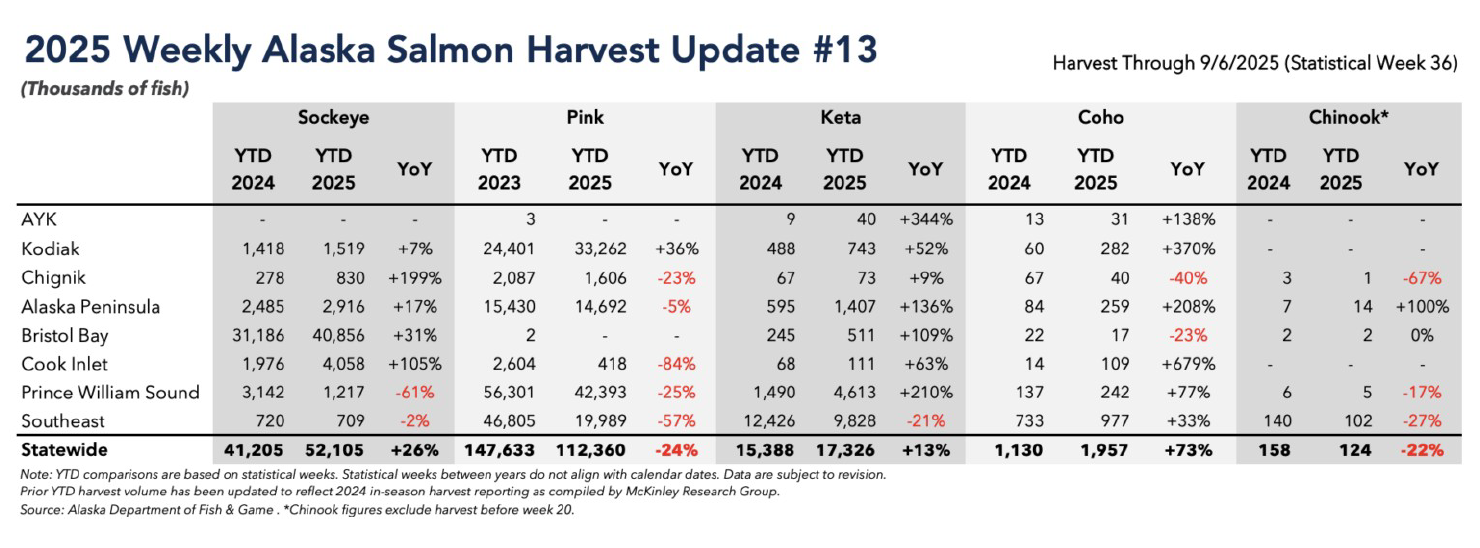

The final weekly salmon harvest update from the Alaska Seafood Marketing Institute (ASMI), offering catch data through Sept. 6, revealed mixed results during the 2025 season.

Though catches were generally poorer this year outside of Bristol Bay, significant runs in the world’s largest sockeye fishery provided a crucial backstop for a sector badly in need of a measure of stability.

“Obviously, catches were low everywhere except Bristol Bay. The pinks didn’t come in as expected. But [processors] were able to get the pounds sufficient to meet their plans. Everything they have is sold. It’ll take time, obviously, to work through it, and they were hoping it had a been better [season all-round], but they’re in OK shape,” said the source, who requested anonymity.

While the sockeye run wasn’t universally great, with poor returns in a few areas, fish sizes returned to higher averages and the runs came in over a longer duration, unlike in previous years, where processors have been jammed and intake times stretched out, resulting in a drop in product quality, he said.

Importantly, processors were in better shape to maximize the good season, the source said.

“The fact that the industry in Alaska went into the salmon season in such a better place helped a ton,” the source said. “There wasn’t a huge inventory carryover. There was pretty solid demand from buyers and the prices buyers were willing to pay was up over the last couple of years.”

Still, Alaska’s salmon industry is still very much in transition, the source said.

“I would not say we’re set at a new normal yet,” he said. “There are still some moving parts out there.”

Big three

After the major realignment of the industry through lean years beginning in 2022, the three largest survivors — Silver Bay Seafoods, Trident and Canadian Fishing Company (Canfisco) — remain the dominant players. However, consolidation may continue, the source said, as there’s a near-universal realization now that there’s no easy money to be made in Alaska’s salmon industry.

“We had two very brutal years that triggered some massive changes in Alaska. 2022 was a bad year, but people had hoped it would bounce back in 2023 and they would be fine. After another bad year, it just got to where people realized they couldn’t do it anymore. They couldn’t count on running plants that didn’t make money, or that only made money every third year,” the source said.

“That willingness to be honest with themselves about their reality is what drove a lot of those changes, like what happened with Peter Pan disappearing and Trident selling out. And I don’t think we’re through this transition period, because people are really making business decisions now, instead of just hoping things will get better next year.”

There are two pathways to success in Alaska’s current-day salmon industry: through size or specialization, he said.

“Being big and having all that scale is one way to be successful in Alaska, while the other is grabbing a niche and being a specialist that does one thing very well and makes a name for themselves doing it,” he said.

Copper River Seafoods, an Anchorage-based processor with five facilities across Alaska, is a good example of “a company that has a brand and stays in its lane,” the source said.

The company, which operates its own branded salmon line sold in grocery retailers and through direct-to-consumer online marketing services, won the state’s 2023’s Manufacturer of the Year award for its innovative efforts to better utilize salmon byproducts and offcuts

“But being a medium-sized firm that’s in a couple of locations hoping to meet their demand, I just don’t think that works anymore,” the source added.

Nowadays, there are very few companies actively looking to grow, he said, and several who would sell.

“I think there are still folks open to getting out and if they could get the right price, they would,” the source said. “I know of a couple little guys who would love to partner with somebody bigger. Some are still barely making it.”

The source named online sales specialist Wild Alaska Company as a sole exception. The Homer, Alaska-based company, launched in 2017, made two big hires recently in a big step toward breaking more into retail and foodservice sales, as reported by Undercurrent.

“They’ve made a couple of moves and talked a little bit about possibly becoming more vertically integrated. So maybe they would be somebody who might be interested in a plant or something,” he said.

“But otherwise, most people are either are good with what they’ve got or wouldn’t mind having fewer assets. Maybe Wild Alaska takes advantage of that and enters a partnership or perhaps they get a plant or two in a couple key locations to just control their own supply.”

Trident’s scaleback

Trident, while still one of Alaska’s biggest processors, initiated a comprehensive restructuring initiative in 2023 that involved the sale of four of its Alaska shoreside plants, among other moves, as Undercurrent reported at the time.

While still a major player, Trident’s move to downsize its Alaska footprint came as a surprise to some, but the decision was purely financial, according to the senior banking executive.

“My sense about Trident is they just looked around and said, ‘You know that location, we make money there once every few years, and maybe that’s not good enough anymore,'” the source said. “That plant or vessel we’ve owned for decades, we don’t use it or we don’t make money regularly, and it’s not worth paying the mortgage anymore.

They got to a point where they decided if not worth opening it, they should just cut back. They started making business decisions around where to operate.”

Others have made similar moves, just on a smaller scale, the source said, “but that maybe got overshadowed because Trident is just so big that they get all the attention.”

Trident remains a massive global player, but its identity has shifted from being an Alaskan seafood company to a value-added firm, Mark Working, the co-founder and managing partner of Zachary Scott, a Seattle-based boutique investment bank that provides mergers and acquisitions, capital advisory and strategic financial consulting services to privately held middle-market companies, including many in Alaska’s seafood industry, agreed.

“After growing across many fisheries and international sales channels, Trident undertook a strategic realignment of its businesses to allow it to focus on its value-added products and areas where it can sustainably compete internationally. Ultimately, it had to make a choice and viewed its commodity salmon operations as the least supportive of its competitive position,” Working recounted.

Quality investments

Following an acquisition streak that included purchases of rival OBI Seafoods and Trident’s Ketchiken plant, Silver Bay Seafoods is now widely regarded as the “big kahuna” of Alaska’s salmon industry.

Adding to its riches, Silver Bay Seafoods was set to acquire all of its struggling rival, Peter Pan Seafoods, after the 2024 Alaska salmon season, having inked a deal to acquire one of its plants and operate two more.

However, while Peter Pan’s assets were sold via a forced receivership process, many of them ended up in the hands of Peter Pan’s former owner, Rodger May, who beat out Silver Bay in an auction process in September 2024, as Undercurrent reported.

Now, there are unresolved ownership issues between Silver Bay and Peter Pan, as reported by Undercurrent, clouding the short-term future of processing plants in Port Moller, Dillngham and King Cove.

However, with Silver Bay’s other big moves, the operational landscape of the industry is largely set for coming years, the bank executive said.

Silver Bay and Trident have been joined by Canfisco as the three big players in Alaska salmon industry. Canfisco, part of the sprawling $10 billion turnover Jim Pattison Group, Canada’s second-largest private company, acquired a stake in E&E Foods and Alaska processor Big Creek Fisheries in 2020 and 2021, respectively.

Silver Bay now has at least a 60-70% share in processing Alaskan pink and sockeye salmon, while those big three now control 70-80% of Alaskan sockeye salmon processing, one source estimated.

The next few years will see less M&A and more investment in internal improvements to processing capacity, with a focus on quality and using profits to pay down debt, added Working.

“The consolidation has unlocked enough profit margin that the industry can invest in itself again,” he said. “Innovation will spawn capital investment to apply greater automation and new technologies and systems to lower costs and improve quality. Further plant-level consolidation is likely, although within entities, as new highly-efficient plants will replace old infrastructure. With all the indirect costs having been squeezed out, direct production efficiency is the only remaining path to higher profits and a sustainable future.”

Those who can figure out the quality game will be the most successful moving forward, Working said, with floating processors Northline Seafoods and Circle Seafoods, described as “R&D experiments,” good examples to follow.

The two Washington state-based firms just finished up their first full seasons operating floating freezer barges, having been launched in 2024 with the idea of improving the quality of the salmon they process by speeding up the time between catch and freezing, as Undercurrent reported.

“There is some real sound experience that’s being developed there that will end up showing the industry a way to get better quality,” Working said. “They’re small relative to the whole industry there, but I hope they will become more than that.”

The view that M&A action is likely to be limited in the near-term future is shared by C.J. Arrigo, a director at Antarctica Advisors, a specialist strategic advisory service for the global seafood industry.

“The industry is not far out of a pretty tough storm, and now there’s all this economic instability with the US tariffs,” he said. “I think everyone is going to going to catch their breath, take stock, evaluate where they stand and then figure out how they want to move forward,” he said.

There is consensus that those who escape the commodity trade will fare best, according to Arrigo.

“Everyone wants to capture more margin and is figuring out how to do that,” he said. “Clearly, you’ve seen some of the first movers already, and that’ll spread. The lights are coming on, but it’s not going to be overnight.”

Jana Singleton, a senior vice president with Bank of America, who works closely with the seafood industry in the Pacific Northwest, said the next few years will bring less big-ticket mergers and acquisitions and more internal plant investments.

“Capital expenditures in plants getting retrofitted or getting new equipment are definitely less costly than building a full-scale new salmon processing plant. Any new-build plant in Alaska at this point is a monumental task that faces hurdles despite the long-term benefit,” Singleton said.

Long haul

While piecemeal, infrastructural investments would be proof that the industry is willing to be on the future of the salmon biomass in Alaska, which may be becoming less predictable due to climate change and other human-caused phenomena.

“People in the industry are not overly concerned with the unpredictability of the runs lately,” Working said.

“It’s just a super-risky business, and most of the people in the business are really steeped in it and understand it. If you can’t live with that, then you’re never going to invest in the industry.

That’s one of the reasons why you haven’t seen much outside money come into the Alaska seafood industry. Investors get intrigued by it, but then realize it’s much different than what they thought it would be.

“There is no real growth in the industry, only chances for innovation to become more efficient.”

Only the big three salmon players are of any possible interest to outside investors, he said.

“Possibly now that the remaining participants are large, there may be more stability and investors might look differently at these companies,” he said.

Despite the frequent use of the word “unprecedented” to describe the current situation facing the global seafood industry, there are rich historical lessons from Alaska’s salmon sector from which today’s operators can draw.

“The gut-wrenching reformation of this industry meant a lot of money was lost and gained, with a majority of the parties in the ‘disappointment’ column,” Working said.

“It is not unique in its evolution, and it’s difficult to say what the next 25 years will bring. If we can learn anything from our front-row seat, it’s that the survivors saw the writing on the wall and took action when they could, instead of when forced to. Things that can’t continue forever won’t, and being on the right side of the cost equation matters.”

SOURCE: Undercurrent News